Is the cap-weighted S&P 500 Total Return Index getting to be too concentrated for some investors?

Maybe!

Should a fiduciary be concerned?

Probably!

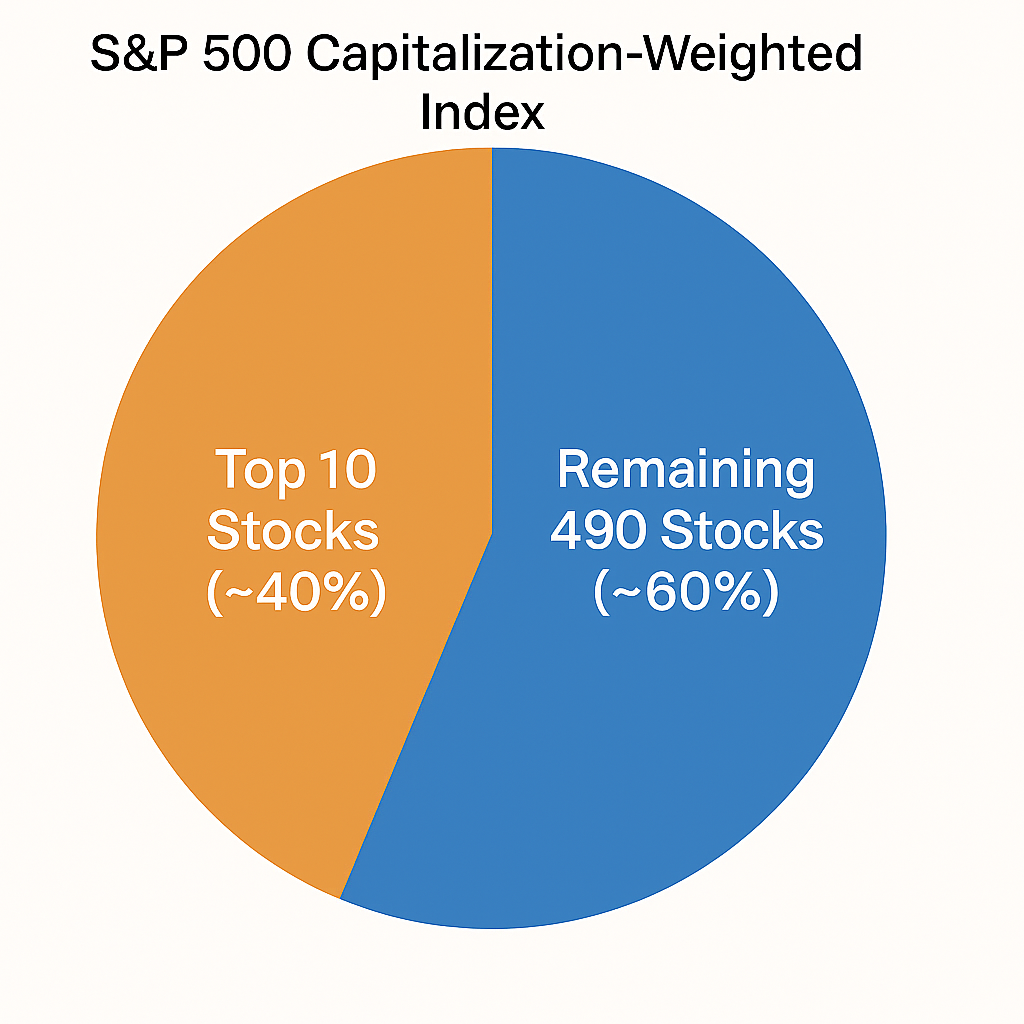

In 2025, the 10 biggest companies in market value accounted for about 40% of the S&P 500 total return.

Also in 2025, just three companies, Nvidia, Apple and Microsoft, accounted for about 21% of the S&P. The next seven brought the total to about 40%.

7.70% - Nvidia

6.20% - Apple

5.90% - Microsoft

5.80% - Alphabet

3.90% - Amazon

3.30% - Berkshire Hathaway

2.60% - Broadcom Inc.

2.40% - Meta Platforms

2.10% - Tesla

1.50% - Eli Lilly & Co.

The three biggest companies are all part of the same sector, Information Technology. The result is the S&P 500 is both concentrated in three companies, and one sector.

Most people I speak with know the S&P 500 has become concentrated. Reference to the Magnificent 7 is frequently mentioned in the press and has become a popular topic for party small talk.

What is generally not understood is: Concentration in a few stocks has dramatically increased over the past 25 years.

According to the Visual Capitalist, long-term history [1880-2010] shows the top 10 stocks as much less concentrated. The average concentration among the top ten was about 24%. Today, the top three alone represent about 21%. Making concentration even more noteworthy is: They are all in that same information technology sector.

The degree of concentration is rare. Only ten years ago the top three accounted for about 7% of the S&P 500.

In the 1999—2000 dot-com bubble, we did see a similar concentration of about 20% in the top three companies, but only two of the three were in the technology sector.

Another way to look at concentration is to break down the S&P 500 into three separate categories.

1) Companies that increased their market value at least as much as the broad index (about 31% of companies).

2) Companies that increased more than 0 but less than the index which was up 17.9% (also about 31%).

3) Companies that decreased in value and had negative returns lower than 0 (about 38%).

We expect the number of stocks significantly contributing to the total return of the S&P 500 to expand over the next few years. In other words, the top 20 stocks will contribute closer to the historical norm of 20%, not the current 40%.

How the adjustment may occur is, of course, the question. It is possible the new normal will have increasingly fewer stocks dominating the index. In that case, the stock market will move forward as it has been over the past few years. The other possibilities include a gradual adjustment to the historical norm, or possibly a fast and violent adjustment.

For now, we are “staying the course”.

We thank you for allowing us to be your trusted financial advisor. Please contact your Private Wealth Manager with any questions. A discussion with Kevin or me can be arranged to cover our investment strategies and review your asset allocation.

Best,

Tom Curran

Founder & Co-CEO

Curran Wealth Management

At Curran we value service over sales and believe quality service yields happy clients. Below is our 4-step process (the first three steps at no cost to you).

A short introductory call for us to get to know one other. During this call we will discuss your financial goals, concerns and hopes for the future.

In this meeting we will go over your current financial situation, take a deeper look at your goals, discuss your risk tolerances, and collect the data necessary to build a formal proposal.

Based on our data gathering session, our Private Wealth Managers will present you with a custom proposal tailored to your needs. We encourage individuals to take the time to evaluate this proposal.

If you are comfortable with the proposal and choose to invest with Curran, our team will be there every step of the way assisting in opening the recommended accounts and facilitating all necessary parts of your onboarding process.